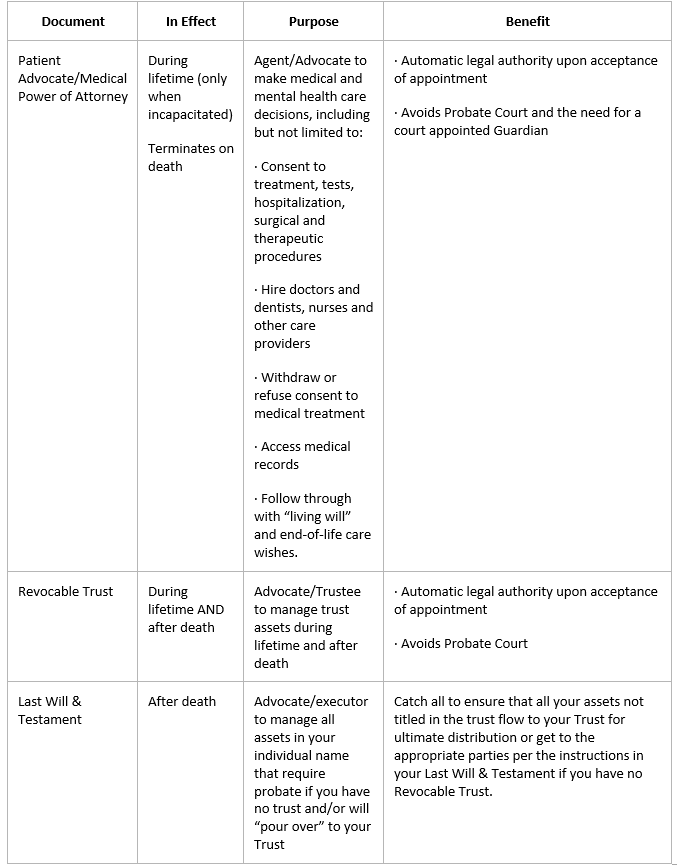

Contributed by: Sandra Adams, CFP®

Contributed by: Sandra Adams, CFP®

My grandmother died recently. She was 96 (almost 97) years old. The leading cause of death listed on her death certificate was Alzheimer’s disease. The last years of her life were not what I would call the best of “quality” – she had not been able to get out of bed to walk for several years, and while she did recognize her children until the end of her life, she would forget they had been there to see her within minutes. She outlived all of her siblings and most of my grandfather’s siblings (and my grandfather by almost three decades) and had been saying she was “ready to go” for quite some time.

Most of us familiar with Alzheimer’s and related dementias know that there are many types, and it is often hard to diagnose, especially if there are other health concerns. For many, it is more a result of older age than genetics; for those where early onset can be an issue, the symptoms can be masked by stress or other mental health issues, and the dementia can go untreated for years. Alzheimer’s and dementia causes and treatments are making some real progress but remain more of a mystery than they should for the more than 5.5 million Americans living with the disease.

While we are still being told that only a small fraction of those developing the disease are those that are not inherited (1 in 100 according to the Alzheimer’s Association), witnessing my grandmother spend her last several years in a nursing home floor of a hospital prompted me to make sure I had my Long Term Care plans covered.

When my grandparents were my age, Long Term Care insurance was unavailable. And because of that, my grandmother ended up spending down the assets my grandfather worked so hard for during his working life and living out her last years in a hospital nursing home on the memory care floor. She was fortunate to have ended up where she did — she was so well taken care of in a small town hospital. Some people don’t have it so well.

I want to make sure to have more control if this happens to me — and want to make sure that I can afford for care to be provided for me (rather than to have my kids have to do it), so I recently took steps to make sure I have a long term care policy in place that suits my needs. I am taking care of this now to have a plan in place for later.

As I tell clients all of the time, many of us don’t feel it is important to take action until we have had a personal experience with something. For me, watching my grandmother experience Alzheimer’s and Alzheimer’s care for the last several years has prompted me to put a Long Term Care plan into place for myself. If you have had a personal experience prompting you into action and would like our help, please do not hesitate to reach out — we are always happy to help!

Sandra Adams, CFP®, is a Partner and CERTIFIED FINANCIAL PLANNER™ professional at Center for Financial Planning, Inc.® and holds a CeFT™ designation. She specializes in Elder Care Financial Planning and serves as a trusted source for national publications, including The Wall Street Journal, Research Magazine, and Journal of Financial Planning.

Any opinions are those of Sandra D. Adams, CFP® and not necessarily those of Raymond James.

Securities offered through Raymond James Financial Services, Inc., member FINRA/SIPC. Investment advisory services are offered through Center for Financial Planning, Inc. Center for Financial Planning, Inc. is not a registered broker/dealer and is independent of Raymond James Financial Services. As with most financial decisions, there are expenses associated with the purchase of Long Term Care insurance and policies are subject to exclusions and limitations. Guarantees are based on the claims paying ability of the insurance company.